.svg)

What Is a Manufactured Home? Guide for First-Time Buyers

If you have ever searched "what is a manufactured home" while scrolling through real estate listings late at night, you are not alone. Millions of Americans are asking the same question as home prices continue to climb well out of reach.The median single-family home in the U.S. now tops $367,000, and for many first-time buyers, that number feels less like a goal and more like a wall.

Manufactured homes offer a real and well-regulated alternative, one that is worth understanding fully before you write it off or rush into it.This guide walks you through everything you need to know, from the legal definition and construction standards to financing, appreciation, and the costs most buyers don't see coming.

What Is a Manufactured Home?

A manufactured home is a residential dwelling built entirely inside a climate-controlled factory and then transported to its permanent site, either a private piece of land or a spot within a land-lease community. Unlike a site-built home that goes up board by board on a construction lot, a manufactured home arrives nearly complete, typically in one or two large sections that are joined on-site.

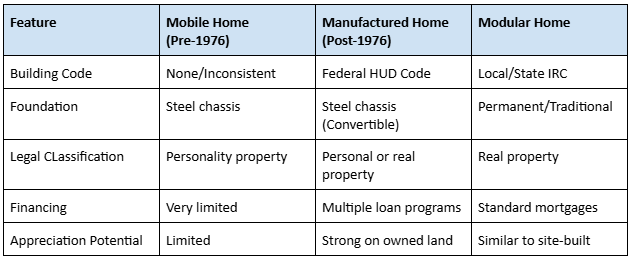

The legal definition is specific. According to the U.S. Department of Housing and Urban Development (HUD), a manufactured home must be at least 320 square feet and constructed on a permanent steel chassis. That chassis is what physically distinguishes a manufactured home from every other type of factory-built housing.

It makes transportation technically possible, though in practice, most manufactured homes are set in place and never moved again. The term "manufactured home" is not a marketing upgrade from "mobile home."It is a separate legal classification that came into existence on June 15, 1976, the day HUD's Manufactured Home Construction and Safety Standards, known simply as the HUD Code, officially took effect. Homes built before that date are classified as mobile homes and are not subject to a consistent federal safety standard.

Everything built after June 15, 1976 falls under the manufactured home category, with all the protections and financing eligibility that come with it.

What Is the Difference Between a Manufactured Home, a Mobile Home, and a Modular Home?

This is the question that creates the most confusion for first-time buyers, and the mix-up is not just semantic. Getting these three categories wrong can directly affect the type of loan you qualify for, the insurance you can get, and the resale value of the home.

A mobile home was built before 1976. These homes were constructed without a uniform federal safety standard, which makes them harder to finance, insure, and title in many states.

A manufactured home was built after June 15, 1976 under the federal HUD Code, which sets minimum standards for structural integrity, fire resistance, energy efficiency, electrical systems, and plumbing. A modular home is also factory-built, but must comply with local and state building codes rather than the federal HUD Code.

Modular homes are placed on traditional permanent foundations, which makes them legally identical to site-built homes the moment construction is complete.

The distinction between modular and manufactured homes matters most when you apply for a mortgage. A modular home qualifies for a conventional mortgage right away. A manufactured home requires a specialized loan program unless it has been formally converted to real property status.

How Did the HUD Code Change What a Manufactured Home Is?

To fully understand what a manufactured home is today, it helps to understand what it was before 1976. The mobile home industry before that point had almost no guardrails. Construction quality varied wildly from one manufacturer to the next.

Fire safety was inconsistent at best, and buyers had very little legal recourse when a home fell apart or proved dangerous. Congress passed the National Manufactured Housing Construction and Safety Standards Act in 1974, directing HUD to develop and implement a national standard by mid-1976.

The resulting HUD Code covers structural design, fire resistance, energy efficiency, electrical systems, plumbing, and even the way homes are built to withstand transportation. The Code does not sit still. It is regularly updated by the Manufactured Housing Consensus Committee, a body composed of manufacturers, consumers, public officials, and general interest representatives.

This means the standard continues to reflect current construction science and safety research.

What Types of Manufactured Homes Can You Buy?

Once you understand what a manufactured home is, the next step is understanding the configurations available and what each one means for your budget and lifestyle.

• Single-wide homes run 14 to 18 feet wide and range from 400 to 1,800 square feet. With an average price around $84,900, they are the most affordable starting point and work well for individuals, couples, or buyers with a tighter budget.

• Double-wide homes consist of two factory-built sections joined on-site. They span 20 to 36 feet wide and typically offer 1,000 to 2,500 square feet of living space. At an average price of around $145,700, they deliver a layout that feels very similar to a traditional ranch-style home.

• Triple-wide and multi-section homes are designed for larger households or buyers who want more space and more modern features. These homes can exceed 3,000 square feet and often include vaulted ceilings, open floor plans, kitchen islands, and upgraded finishes.

It is worth addressing the design question directly. Many people who research what a manufactured home is expect dated, cramped spaces.The reality in 2026 is quite different. Modern manufactured homes are built with low-E windows, solar-ready roofing, ENERGY STAR appliances, smart HVAC systems, and sustainable building materials.

Because construction takes place in a controlled factory environment where temperature, humidity, and materials are closely managed, the building process can produce tighter seals and better insulation than homes built outside in variable weather conditions.

How Much Does a Manufactured Home Cost?

The price difference between a manufactured home and a traditional site-built house is substantial. In 2024, the average manufactured home sold for $123,300, compared to the median single-family home price of $367,282. That is roughly 66% less expensive on the purchase price alone.

However, the purchase price is only part of the story. First-time buyers who do not account for the full cost of ownership are often surprised when the bills start arriving. Here is what a realistic total cost picture looks like:

• Home purchase price: $84,900 to $145,700 or more, depending on size and features

• Land purchase or monthly lot rent: Lot rent in communities typically runs $300 to $1,000 per month

• Site preparation and foundation work: $5,000 to $30,000 or more

• Utility connections for water, sewer, and electric: $3,000 to $15,000

• Transportation and installation: $5,000 to $15,000

• Permits and closing costs: $1,000 to $5,000

The single biggest financial trap in manufactured home buying is lot rent. If you place your home in a land-lease community and pay $700 per month, that adds up to $84,000 over 10 years, more than the purchase price of many single-wide homes.Buyers who understand this upfront almost always weigh private land ownership more seriously before committing to a community.

How Do You Finance a Manufactured Home?

Financing is where the question of what a manufactured home is becomes very practical. The loan options available to you depend on a single classification: is your home real property or personal property?

Real property means the home is permanently affixed to land you own and has been formally titled as real estate. Personal property, often financed through a chattel loan, means the home is treated more like a vehicle than real estate.

This classification has a major impact on cost. As of early 2025, chattel loans carry interest rates of 8% or higher, while the average 30-year fixed-rate mortgage runs around 6.76%. Chattel loans also come with higher denial rates, approximately 66% compared to 43% for real-property loans. Over a 20-year loan, that difference in interest rate translates into tens of thousands of dollars in additional costs.

The main loan programs available to manufactured home buyers include:

1. FHA Title I and Title II Loans

Government-backed loans with down payments as low as 3.5%. Title I is for homes on leased land; Title II requires a permanent foundation on owned land.

2. VA Loans

For eligible veterans and active-duty service members, often requiring no down payment.

3. USDA Loans

Designed for rural placements on owned land, with zero-down options available.

4. Chattel Loans

The most common type is used for homes on rented land. Rates range from 5.99% to 12.99%, terms run up to 20 years, and down payments are typically 20 to 30%.

Over 40% of manufactured home purchases are financed through chattel loans. If building equity and managing long-term costs are priorities for you, pursuing real-property classification from the start, or buying land alongside the home, is almost always the smarter financial move.

Do Manufactured Homes Appreciate in Value?

One of the biggest misconceptions about manufactured homes is that they always lose value. That belief is outdated and not backed by current data.

Analysis of Federal Housing Finance Agency data by the Urban Institute found that manufactured homes appreciated at nearly the same rate as site-built homes between 2000 and 2024, growing approximately 5% per year on average.

Over that 24-year period, site-built homes appreciated 212.6% while manufactured homes appreciated 211.8%. Since 2014, manufactured homes have actually outpaced site-built home appreciation in nearly every quarter on record.

The condition that makes appreciation possible is land ownership. Manufactured homes in land-lease communities, where homeowners pay monthly lot rent but do not own the land, tend to build equity more slowly.

That is not unique to manufactured housing. Any home on land not owned faces the same dynamic. The average price of a new manufactured home rose from $82,400 in 2018 to $123,200 in 2024, a clear signal of growing market demand.

How Long Does a Manufactured Home Last?

A well-maintained modern manufactured home is built to last 30 to 55 years, and many exceed that with proper care. Pre-1976 mobile homes carry a different expectation because they were built without consistent federal standards.

Post-1976 manufactured homes are a different category entirely, constructed to meet HUD Code requirements that directly address structural durability, fire resistance, and long-term performance.

Three factors shape how long a manufactured home lasts: the quality of the foundation, the local climate, and the level of maintenance. Homes on permanent foundations in moderate climates, with attentive owners, regularly outlast their rated lifespans.

Moisture intrusion is the most common cause of early deterioration, making roof maintenance, caulking, and proper ventilation high-priority tasks for any manufactured homeowner. The factory construction process itself offers a durability advantage that many buyers overlook.

On a traditional construction site, building materials are exposed to rain, humidity, and temperature changes before the home is finished. In a factory, those variables are controlled throughout the entire build, which typically results in tighter construction and more consistent material performance.

Who Is Buying Manufactured Homes Today?

The buyer profile for manufactured homes has changed considerably. There are currently 7.2 million occupied manufactured homes in the United States, accounting for 5.4% of the total occupied housing stock.

Shipments reached 103,300 units in 2024, and the annualized rate had risen to 106,000 by mid-2025. The U.S. manufactured housing market is valued at approximately $14.6 billion in 2026 and is projected to reach $19.8 billion by 2031, reflecting a compound annual growth rate of 6.28%.

Manufactured housing has historically served rural and lower-income households, and it continues to do so. But the buyer pool now includes first-time buyers priced out of urban and suburban markets, retirees looking to reduce housing costs without sacrificing comfort, and real estate investors acquiring manufactured home communities as income properties.

Texas, Florida, and North Carolina recorded the highest total shipments in 2024, while Mississippi, Kentucky, and Louisiana had the highest concentration of manufactured homes as a share of all new single-family housing.

Conclusion

Understanding what a manufactured home is goes well beyond a dictionary definition. It means recognizing a housing option that is federally regulated, built to consistent national standards, and in many cases, just as capable of building long-term equity as a traditional site-built house.

The numbers tell a straightforward story. At an average purchase price of $123,300 compared to $367,282 for a site-built home, the affordability gap is real and significant. Appreciation data from the Urban Institute shows that manufactured homes on owned land appreciated at nearly the same rate as site-built homes over a 24-year period. The stigma attached to this housing type has not kept pace with the reality of modern manufactured homes.

That said, this is not a purchase to make on impulse. The difference between a good outcome and a costly one often comes down to three decisions: whether you own the land, how the home is titled for financing purposes, and whether you account for all the costs beyond the purchase price. Get those three things right, and a manufactured home becomes one of the most practical and financially sound housing choices available to a first-time buyer today.

If you are exploring manufactured homes for sale in Michigan, the right community partner makes a significant difference in how the process goes. MCM Communities has helped Michigan residents find well-built, affordable manufactured homes in communities designed for long-term living.

Whether you are just starting your search or are ready to take the next step, their team can walk you through available homes, community options, financing guidance, and everything else you need to make a confident decision.Contact MCM Communities today to learn more about manufactured homes for sale in Michigan and find out how they can help you move from searching to settled.

The path to homeownership does not have a single starting point. For many Michigan residents, it starts with the right conversation and arrives as something worth calling home.

FAQs

What is a manufactured home vs. a mobile home?

A mobile home was built before June 15, 1976, without consistent federal safety standards. A manufactured home was built after that date under the HUD Code, which sets national minimum standards for construction, fire safety, energy efficiency, and structural integrity. The two terms are often used interchangeably in casual conversation, but they refer to legally and structurally different things.

What is the difference between a HUD Tag and a HUD Data Plate?

The HUD Tag is a small metal plate on the exterior of each home section that confirms it was built to federal HUD standards. The HUD Data Plate is an interior document listing the home's specifications, including wind zone, thermal zone, and roof load capacity. Both are required for most loan programs and should be present on any pre-owned manufactured home you consider buying.

Can you get a traditional mortgage on a manufactured home?

Yes, if the home is permanently affixed to land you own and has been titled as real property. FHA Title II, VA, and USDA, all offer mortgage-style financing for manufactured homes that meet specific requirements.

Are manufactured homes safe in severe weather?

Modern manufactured homes are built to zone-specific wind standards under the HUD Code: Zone I for standard conditions, Zone II for moderate-risk areas, and Zone III for high-risk, hurricane-prone coastal regions. A properly anchored home built to the appropriate zone standard meets federal safety requirements for its regional weather conditions.

How long does it take to move into a manufactured home?

Because factory production is not affected by weather delays or on-site construction variables, a standard manufactured home can go from order placement to move-in in 60 to 120 days. That is significantly faster than the 7 to 12 months typically required for new site-built construction.